Introduction to TDS

TDS stands for Tax deducted at source. TDS is also known as withholding tax, and It is not a separate tax, it is just a method of tax collection adopted by the government. It is a part of Income Tax and hence governed by Income Tax Act 2058, hereinafter referred to as Act.

As the word suggests, TDS is the amount deducted from the source of income generation and paid to the government. TDS amount needs to be deducted at the time of

- Making a payment to the service provider or

- Recording the expense in the account books by the service receiver

whichever is earlier.

Let’s learn more about its Applicability:

There are four major categories in which TDS is applicable:

A. Salary including any monetary allowance paid to an employee

B. Payment of Service Fee and Investment Return which includes the following:

- Interest by banks or financial institutions

- Rent Payment to a business entity

- Royalty payment

- Payment for other Service Fee

- Payment of Commission or Sales Bonus

- Payments for rights to extract natural resources

- Retirement Payment from Approved or Unapproved Retirement Fund

- Any other Investment Return (Mutual Fund, Dividend, Life Insurance)

C. Payment of Windfall Gain (Lottery, Prize on contest)

D. Contract Payment (Construction, Supply of Human Resources and Goods, etc)

Rates of TDS deduction in Nepal

| S.No. | Transactions | Rate (FY 79/80) |

|---|---|---|

| A. | Salary including any monetary allowance paid to an employee | Slab Rate |

| B. | Payment of Service Fee and Investment Return | |

| (i) | • Interest by banks or financial institutions to foreign banks or financial institutions | 10% |

| • Interest by banks or financial institutions other than above | 5% | |

| (ii) | • Rent Payment for vehicle rental service to VAT registered Service Provider | 1.5% |

| • Rent Payment for vehicle rental service to Service Provider, not registered in VAT | 2.5% | |

| • Other lease rent | 10% | |

| (iii) | Royalty payment | 15% |

| (iv) | Payment for other Service Fee | |

| • Registration and other fees to the foreign university | 5% | |

| • Service Provider is registered in VAT | 1.5% | |

| • Service Provider is not registered in VAT | 15% | |

| (v) | Payment of Commission or Sales Bonus | |

| • Commission to nonresident by resident business entity | 5% | |

| • Commission to a resident employee | Forms part of salary and TDS on Salary applicable | |

| (vi) | Payments for rights to extract natural resources | 15% |

| (vii) | Retirement Payment from Approved or Unapproved Retirement Fund | 5% |

| (viii) | Any other Investment Return (Mutual Fund, Dividend, Life Insurance) | 5% |

| C. | Payment of Windfall Gain (Lottery, Prize on contest) | 25% |

| D. | Contract Payment | |

| Payment to Resident Entity if payment amount made within last ten days exceeds Rs. 50,000 (irrespective of the total contract amount) | 1.5% | |

| Payment of insurance premium or commission on re-insurance premium, to Non-Resident Insurance Company | 1.5% | |

| Payment to Non-Resident Person | 5% |

TDS Exempted Payments in Nepal

TDS has to be deducted while making payments covered in the provision of TDS. However, there are certain exceptions where the TDS deduction is exempt. Following are some of such transactions:

- Interest payment to banks and financial institutions. (eg interest in loan)

- House rent payment to a natural person.

- Dividend or interest payment to a Mutual Fund

- Payment of insurance amount by the insurance company on the death of an insured person.

- Payment made by any non-resident person.

(Any person who is present in Nepal for 183 days or more in the period of 365 days is a resident of Nepal) - Payment made by a natural person for his personal expense (not relating to his business).

- Payment relating to any transaction is exempted from Income Tax. For eg. Windfall gains on receiving a national or international prize of Rs. 5 lakhs or less are exempted from income tax so, TDS is not deducted on making such payments.

How does TDS Mechanism work?

We have learned that TDS is deducted at the time of making payment. So, there are two parties involved.

- Withholding Agent (Payer) – Party who is making the payment

- Withholdee (Payee) – Party who is receiving the payment

Let’s understand this with the help of the example below:

ABC Mall Pvt Ltd owns the shopping complex. Adidas Nepal is one of the tenants who pay the monthly rent of Rs. 1 lakh. For the month of Shrawan 2078, Adidas Nepal has to pay rent of Rs. 1 lakh to ABC Mall Pvt Ltd. On the due date, Adidas Nepal will deduct TDS at the rate of 10% (as applicable on Rent Expense) i.e Rs. 10,000, and makes a payment of Rs. 90,000 to ABC Mall Pvt Ltd. Adidas Nepal will deposit TDS so deducted of Rs. 10,000, in Inland Revenue Department as TDS on Rent. It will also file a TDS return where it will mention that TDS has been deducted on payment of rent to ABC Mall Pvt Ltd.

Responsibility of Payer (Adidas Nepal in the given example)

- Calculate and deduct TDS on making payments for certain transactions at the rate specified in the Act.

- Deposit TDS collected in Revenue department within the due date i.e 25th of next month.

- File TDS Return specifying the transaction and payee within the due date i.e 25th of next month.

When to deduct TDS if payment is late?

TDS is generally deducted at the time of making payment for transactions specified in the ACT. However, it is deemed that TDS has been deducted at the time of recording expense in the account books even if payment has not been made.

For example, a Rent of Rs. 1 lakh is due for the month of Ashad 78. However, due to some financial issues, Adidas Nepal makes payment of rent only in the month of Bhadra 78. In this case, Adidas Nepal will book the rent expense of Rs. 1 lakh in the month of Ashad 78 and also book Rs. 10,000 as TDS payable to the government. TDS so booked shall be deemed to have been deducted in the month of Ashad 78, and the due date for compliance of depositing the amount, filing of return will be 25th of Shrawan 78.

How to deposit TDS in Nepal?

The party making the payment is responsible to deposit the TDS amount in a bank account of the Inland Revenue Department. There are different transactions on which TDS is applicable so one should carefully choose the tax revenue codes while depositing the TDS in the Nepal government account.

TDS deducted in a month has to be deposited within the 25th of the next month. One can either:

- Visit a nearby bank (Rashtriya Banijya Bank, Nepal Bank Limited, Nepal Agriculture Development Bank, others as specified by IRD) and deposit cash.

- Or deposit online using IRD Tax Payer Portal.

Step by Step Process of depositing TDS Online:

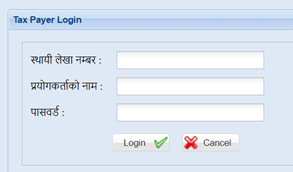

1. Login to IRD Tax Payer Portal using your ID and Password. Your PAN No will serve as your ID.

(If you have not yet activated your ID Password, you can visit your revenue department and apply a form to get your ID and Password.)

2. Click on Payment Voucher.

3. Once you click on Payment Voucher following window will open where you have to fill in the details of the tax deducted. Now fill in the details one by one

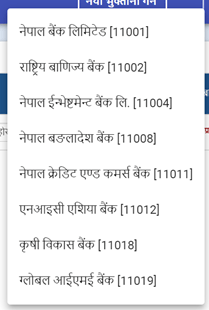

i. Select the bank where you want to deposit the TDS amount. List of Bank that appears might be different for different locations.

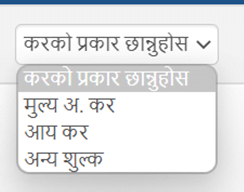

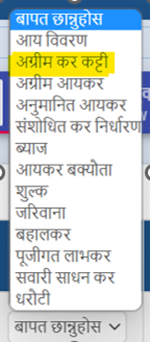

ii. TDS is part of Income Tax so select ‘आय कर’ in first column.

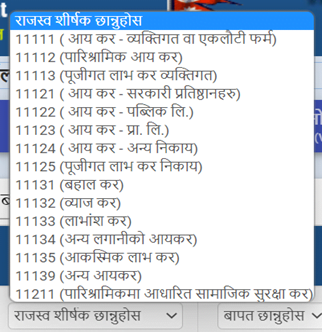

iii. Select the tax type from among the options

| Revenue Code | When to use |

| 11111 | Income Tax relating to an individual or a proprietorship firm |

| 11112 | TDS on Salary |

| 11113 | Capital Gain Tax for Individual |

| 11121 | Income Tax relating to a Government Institutions |

| 11122 | Income Tax relating to a Public Limited Company |

| 11123 | Income Tax relating to a Private Limited Company |

| 11124 | Income Tax relating to Other Entities |

| 11125 | Capital Gain Tax for Business Entities |

| 11131 | TDS on Rent |

| 11132 | TDS on Interest |

| 11133 | TDS on Dividend or Bonus |

| 11134 | Income tax on income from other investments |

| 11135 | Income Tax on Windfall Gain |

| 11139 | Other Income Tax |

| 11211 | Social Security Tax calculated at 1% of salary income |

iv. We are depositing TDS deducted on certain transactions. So select ‘अग्रिम कर कट्टी’

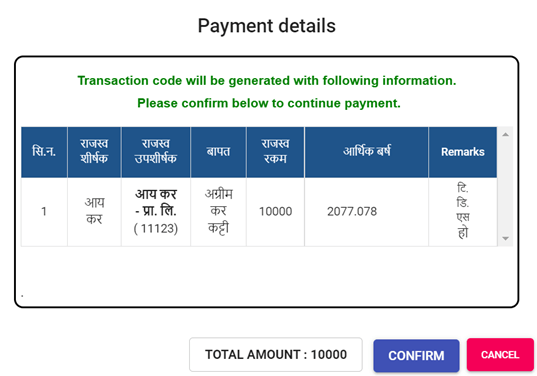

v. Now mention the TDS Amount. (Adidas Nepal would write 10,000.)

vi. Select the fiscal year for which TDS has been deducted. (Adidas Nepal would select FY 77/78 to deposit TDS on Rent for the month of Ashad 78.)

vii. To confirm this is TDS amount being deposited, select ‘हो’

It would look like this when Adidas Nepal would fill the voucher form:

viii. Now to finalize the voucher click on ‘Generate Transaction Code’ lying at the bottom left corner of the screen.

ix. Now the confirmation window will pop up on the screen. Click on Confirm button to generate the transaction code and it will lead us to the payment gateway of connect ips.

x. Now, you can either print the voucher and visit the nearby branch of the bank selected in the voucher to deposit the amount in cash. Or you can make payment online using your connect IPS login credentials.

(It would generally take 1-2 days for the bank to process your payment while online payment would normally take a few minutes to process.)

Read More: EXIM Code Registration in Nepal

How to File TDS Return in Nepal?

Filing of TDS Return is now equally important because without filing a TDS return, a business entity shall not receive a Tax Clearance Certificate.

To file a TDS Return, we need to have voucher details of depositing the TDS amount. If the voucher has been generated online using IRD portal then, voucher details can be viewed in IRD Portal.

Step by Step Process of filing TDS Return in Nepal:

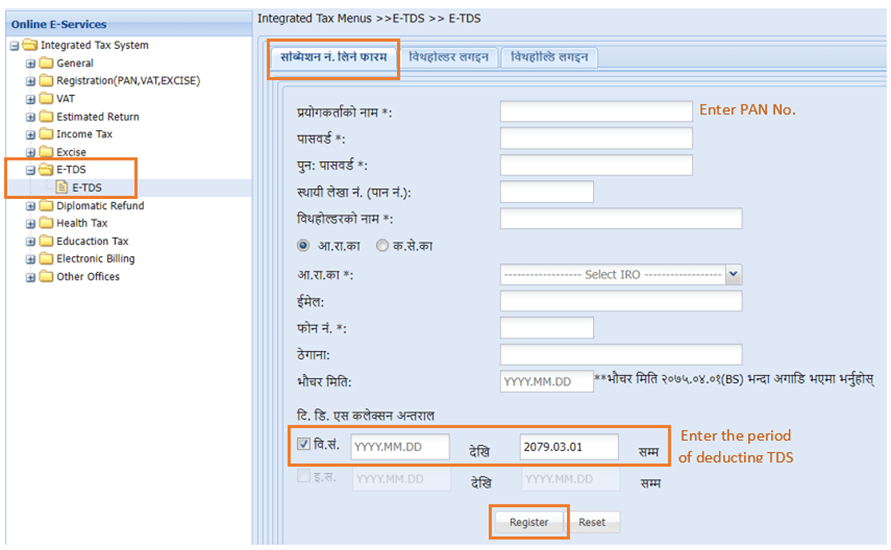

1. Get a Submission No.

Remember, that it is important to generate a submission not to file any return in IRD.

- First, visit Taxpayer Portal on the IRD website. You will get a list of options on the left side of your screen.

- Select E-TDS and further select sub-option E-TDS.

- A form will appear on your screen, which should be filled and submitted to generate a Submission Number.

- Once you get your submission no., save it for future reference.

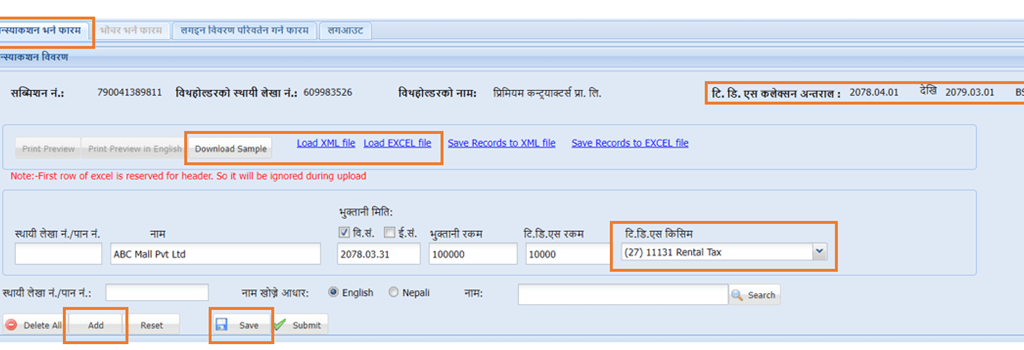

2. Enter Transaction details attracting TDS provisions

The next step is to fill in the details of the TDS deducted.

- Enter the PAN no of the party receiving the amount. Pan No. entered will automatically fill the name of the party.

- If Pan No. is not available, enter the name of the party manually.

- Enter the date of payment in B.S or A.D

- Enter the amount of gross payment made.

- Enter the TDS amount deducted

- Select the Transaction type on which TDS is deducted. This should match with the revenue code used in depositing the TDS Amount.

- If there are multiple transactions to be entered, click on Add button. You can also upload an excel file to enter multiple transaction details instead of manually entering them one by one.

- Click on Save

It would look like this for Adidas Nepal.

3. Once all details are entered. It’s time to enter the voucher details for depositing the TDS amount.

Click on ‘भौचर भर्ने फारम’

- Select the transaction type or revenue code for which voucher detail is to be entered. Here revenue codes relating to transactions entered in the previous tab will be listed.

- Enter the Voucher No. of payment made

- Select the method of deposit: Tax Office, Bank, Online Payment, or Good for Payment Cheque.

- Enter the date of deposit in B.S or A.D. In case the date of deposit is earlier than the receipt confirmed by the department, the date of receipt confirmed should be entered.

- Select the branch of the bank or Tax Office where the deposit has been made.

- Enter the TDS amount deposited.

- Click on Add

- Voucher detail entered should reconcile with the actual voucher processed in IRD. You should not submit until the voucher is shown reconciled.

4. Once all details are entered and reconciled. Click on Submit button in ‘ट्रान्स्याक्शन भर्ने फारम’

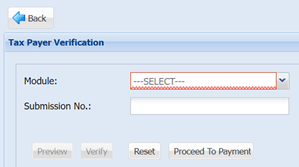

5. Self-Verify the Return

You cannot change or edit the details, Once submitted. If the return filed is wrong, you need to proceed with registering new submission no and submit. This is allowed only if the return has not been verified. This applies to any return filed with IRD.

- Login to IRD Taxpayer Portal using your ID and Password

- Click on Verification

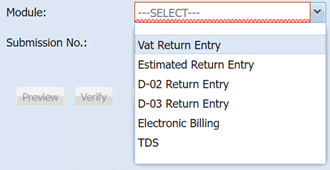

- Select the Module or return that needs to be verified

- Enter the submission no of the return

- Click on Verify button once it becomes activated.

- Once verified, click the Preview button to print or save the return in PDF format.

Impact of TDS on Taxpayers

Let’s see the impacts of TDS on each party involved in transactions covered in the TDS provision.

A. Party making the payment – Compliance Impact

The payer is responsible to deposit TDS and filing the TDS return on the due date. In case of delay, it may have to pay a fine as stated in the Act.

B. Party receiving the payment – Financial impact

The payee will not receive his full payment. A certain part will be deducted as a tax payment to the government. However, this TDS amount can be utilized against the income tax payable.

Read More: Value Added Tax [VAT] in Nepal

How to claim the TDS amount against Income Tax Payable?

The following conditions should be met to claim the TDS amount as an adjustment against income tax payable:

i. Party making the payment (payer) should deduct and deposit the amount with the revenue department.

ii. Party making the payment (payer) should file an e-TDS return. (Introduced in FY 77/78)

TDS deposited can be claimed at the time of filing an income tax return. There is an annexure 10, which automatically populates the TDS details that have been deposited by the withholding agent. This annexure populates the data only if e-TDS has been filed. So, it is important that you ask your payer to file e-TDS at least before you file your income tax return.

Amount populated in annex 10 can be reduced from the total tax liability while making the final payment of tax to the department.

Why was TDS introduced in Nepal?

First, let’s understand why TDS is part of Income Tax.

Income Tax is a major source of government income, but also! final income tax payable will be calculated only after finalizing the profit after the end of the fiscal year. So, to avoid this delay in payment, the government introduced the concept of advance tax that the citizens and business entity needs to pay in installment before the end of the fiscal year.

Also, there is equal chance that business entity evade tax by minimizing the profit in books. So, the government came up with the clever idea to deduct the tax at the time of making the payment itself.

Rate of TDS in Nepal

For different types of services, different rate of TDS is applicable. Some rates of TDS are as follows:

TDS on Salary

There is no fixed rate of TDS deducted on salary. It depends upon the total estimated tax to be paid by the employee.

To calculate the TDS to be deducted following steps are followed:

- Calculate the gross salary

- Estimate annual income

- Calculate annual tax using slab rate

- Calculate monthly tax to be withheld.

TDS on Contracts

The rate of TDS on the contract is also different depending on the amount and time of the payment.

- If the payment is less than 50,000 in moving 11 days: No TDS

- If the payment is more than 50,000 in moving 11 days: 1.5 % of gross income.

- If the payment is more than 50 lakhs at a time: 5% of gross income.

TDS with Income Tax

There are two different natures of TDS. Advance withholding tax and Final withholding tax. The TDS of advance nature is claimed while calculating total income tax at the end of the financial year, whereas in the case of final withholding tax, neither the income is included while calculating tax liability nor the TDS amount can be claimed as tax already paid.

Example,

Marketing Fee = 20,000

TDS deducted = 3000 (Advance Nature)

Net Payment = 17,000

Income tax payable = 55,000

Now,

At year-end:

The Marketing fee of 20,000 is included in the income of the taxpayer, and TDS is deducted, i.e., 3,000 is deducted from income tax payable, and only the net amount is paid to the government.

So, Net Income Tax Payable = 55,000 – 3,000 = 52,000